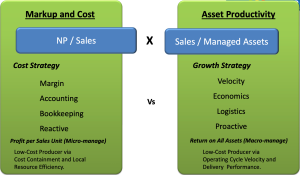

A logistics-centric solution is superior to an accounting-centric cost-cutting approach!

Businesses often miss a financial opportunity that is hiding in plain sight.

For businesses dependent on logistics, manufacturing, MRO, construction, aerospace, and distribution, the real competitive advantage does not come from cutting costs.

For businesses dependent on logistics, manufacturing, MRO, construction, aerospace, and distribution, the real competitive advantage does not come from cutting costs.

It comes from improving how work flows through the system.

But how to prove this in a simple way?

When organizations face pressure—falling prices, rising costs, aggressive competitors—the instinctive response is almost always the same:

Cut costs. Protect margins. Improve resource efficiency.

Yet in practice, this response often leads to the opposite of what leaders intend.

Work piles up, lead times grow longer, delivery becomes unreliable, and managers spend more time expediting than managing. Extended lead times and unreliable delivery place significant pressure on every aspect of the organization.

The organization becomes busier, but not more productive.

Over time, we realized the problem was not just operational—it was conceptual.

We have been measuring productivity the wrong way.

Most organizations define productivity in terms of cost efficiency: reducing expenses, increasing utilization, or improving departmental efficiency.

But the real economic driver of logistics-dependent businesses is something very different:

Asset Productivity. But what is this?

Asset Productivity is a Growth Strategy and Lowers Cost.

Asset Productivity measures how quickly the organization’s assets—facilities, equipment, people, and infrastructure—convert materials and effort into revenue and contribution margin.

When lead times shrink and work flows smoothly through the system, assets become dramatically more productive.

Inventory falls,

asset turnover increases,

cash flow improves,

and even unit costs decline naturally.

In other words, the path to becoming the lowest-cost producer is not aggressive cost-cutting, but maximizing the productivity of the assets already in place.

Years ago, after using a simple financial framework to explain this idea. It revealed something that many operational leaders intuitively understand but struggle to quantify:

Improving logistics performance—especially reducing lead time—has a far greater economic impact than squeezing costs.

The base of which is a logistical economic solution: Asset Productivity.

And once you see productivity through this lens, it changes how you evaluate performance, manage operations, and think about competitive advantage.

Companies that win are not the best cost-cutters.

They are the ones that convert their assets into revenue the fastest.

A Simple Exercise you can perform:

Test the Economics of your Company using the Logistics of Lead Time

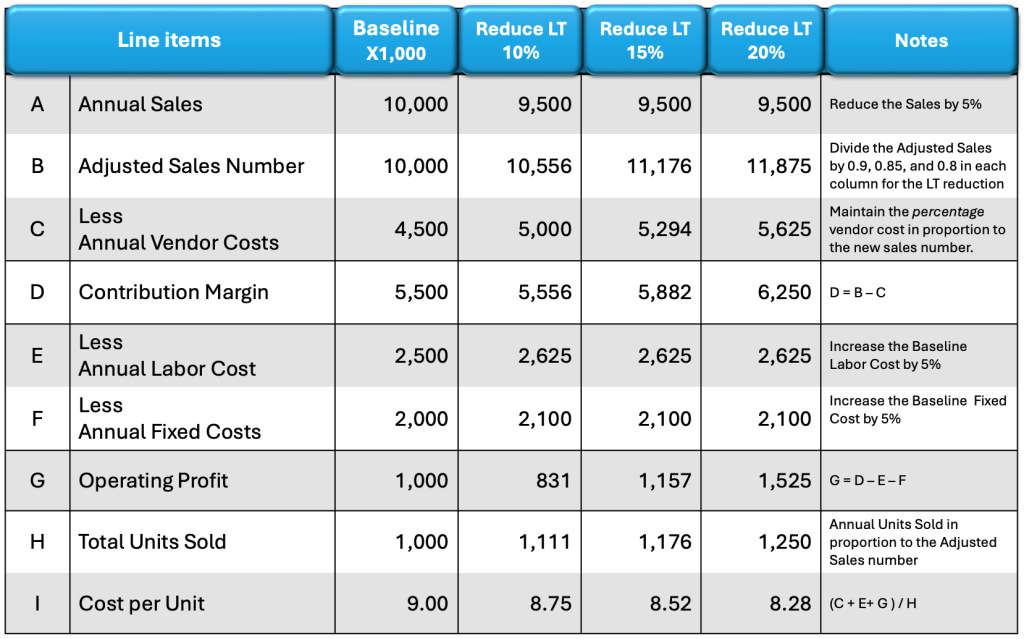

To understand the economic impact of logistics performance, conduct the following simple exercise using your company’s financial numbers.

Start with a margin squeeze scenario—the situation many companies face today.

Figure 1 provides an example to assist with the simple exercise.

- Reduce your current total annual sales price by 5%.

Recalculate your revenue based on this lower selling price. - Using your current vendor cost percentage, calculate the new Contribution Margin based on the reduced sales figure.

- Now simulate cost pressure:

- Increase total annual labor cost by 5%

- Increase all other annual fixed operating costs by 5%

At this point, you have recreated the classic margin squeeze:

- Prices are lower

- Costs are higher

- Margins are under pressure

This is exactly the environment where most companies respond with cost-cutting programs.

But now introduce a different variable.

Using the Margin Squeeze scenario above, improve the logistics performance.

- Reduce your lead time by 10%, 15%, and 20%. Figure 1.

Then apply a simple assumption that reflects what faster flow does in real markets: shorter, more reliable lead times allow you to capture more demand.

To simulate this effect in three different columns:

- Divide your new reduced total sales by 90% for a 10% lead time reduction

- Divide by 85% for a 15% lead time reduction

- Divide by 80% for a 20% lead time reduction

Recalculate the financial results for each of these scenarios using the margin-squeezed baseline—the one where prices were reduced, and costs increased.

Fig. 1

Fig. 1

The Result Is Usually Surprising

There is a downloadable MS Excel Model at the end of this article.

Even under these unfavorable conditions—lower prices and higher costs, but with decreased lead-times—you will typically see something unexpected:

- Profitability increases

- Contribution margin grows in absolute terms

- Cost per unit declines

How is that possible?

Because reducing lead time increases Asset Productivity.

That is, diluting the fixed cost with an increase in transactional volume.

When work moves faster through the system:

- Assets turn over more frequently

- Inventory shrinks

- Throughput increases

- Fixed costs are spread across a greater output

In other words, the system produces more economic value without proportionally increasing cost.

The improvement does not come from squeezing expenses.

It comes from increasing the productivity of the assets already in place.

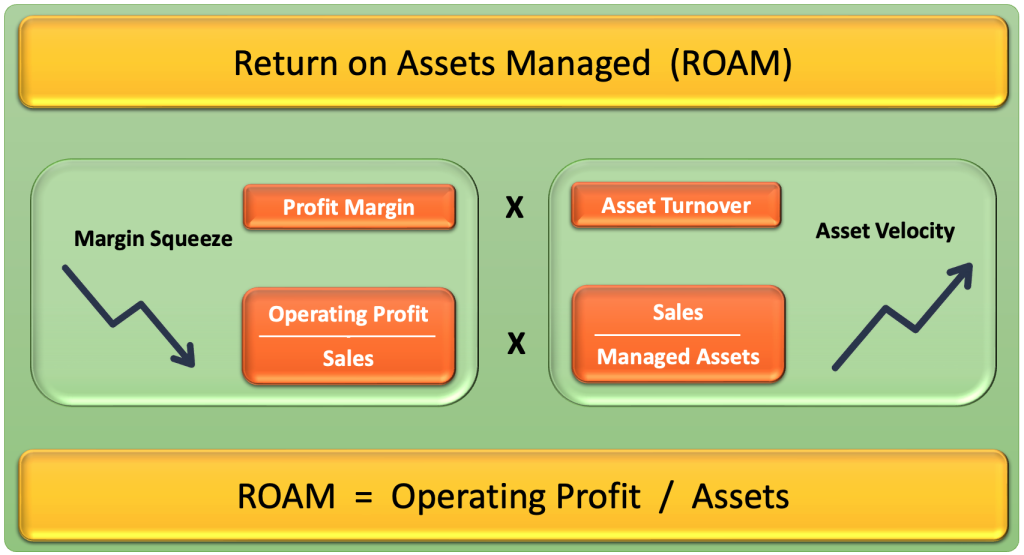

Margin Squeeze on the left side and Asset Velocity on the right side. It is also known as ROAM or Return On Assets Managed. Figure 2.

Fig.2

The Economics of a Logistics Solution

This exercise reveals a critical insight. By focusing on Cost, we are only seeing half of the economic equation.

When companies face a margin squeeze—falling prices and rising costs—the instinct is to manage through cost strategy.

But the cost strategy is accounting-centric. This is only one side of the economic equation. It focuses on protecting margins by reducing expenses.

A logistics strategy, by contrast, is economics-centric.

Asset Turnover(ATO) is the neglected side of the equation.

How fast are the Assets performing relative to the Sales they generate?

ATO focuses on improving flow, shortening lead time, and increasing Asset Productivity—the rate at which assets convert materials and effort into revenue and cash.

And when that happens, something powerful occurs:

- Asset turnover increases

- Contribution Margin or Throughput rises

- Cash flow accelerates

- Unit costs fall naturally

The path out of a margin squeeze is not necessarily to cut deeper into costs.

It is often necessary to increase the system’s velocity.

Rethinking Productivity

This is why the traditional definition of productivity—local efficiency or cost reduction—is incomplete.

The more powerful metric is Asset Productivity: Expressed as Asset Turnover (ATO).

How quickly your assets convert capital into contribution margin.

Once leaders begin measuring productivity this way, the strategic conversation changes.

The focus shifts from:

“Where can we cut costs?”

to transaction velocity:

“How quickly can our system convert work into revenue and Contribution Margin?”

And that shift—from cost efficiency to Asset Productivity—is the foundation of the logistical economic solution.

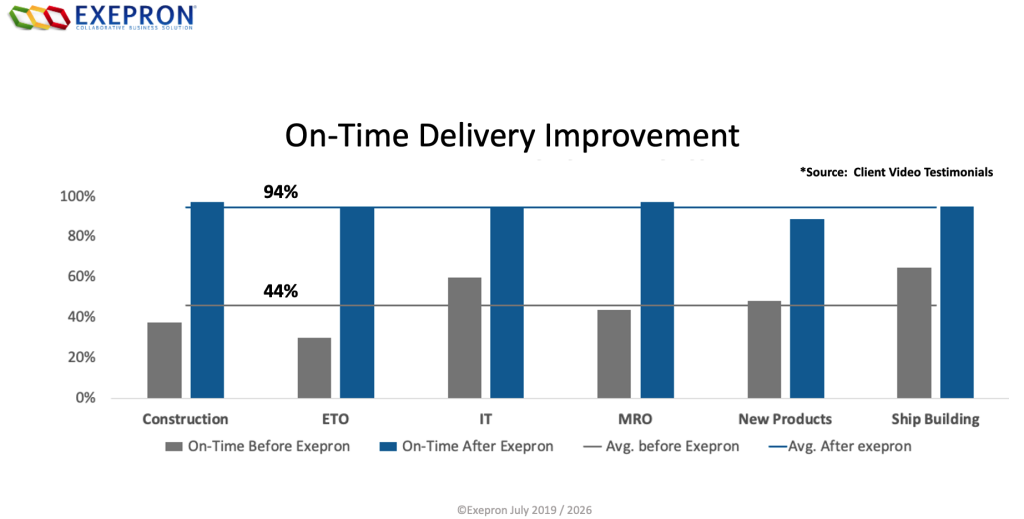

The Opportunity Is Much Larger Than the Example

The exercise above used modest assumptions.

A 10%, 15%, or 20% reduction in lead time is significant, but in many real operations, the potential is far greater.

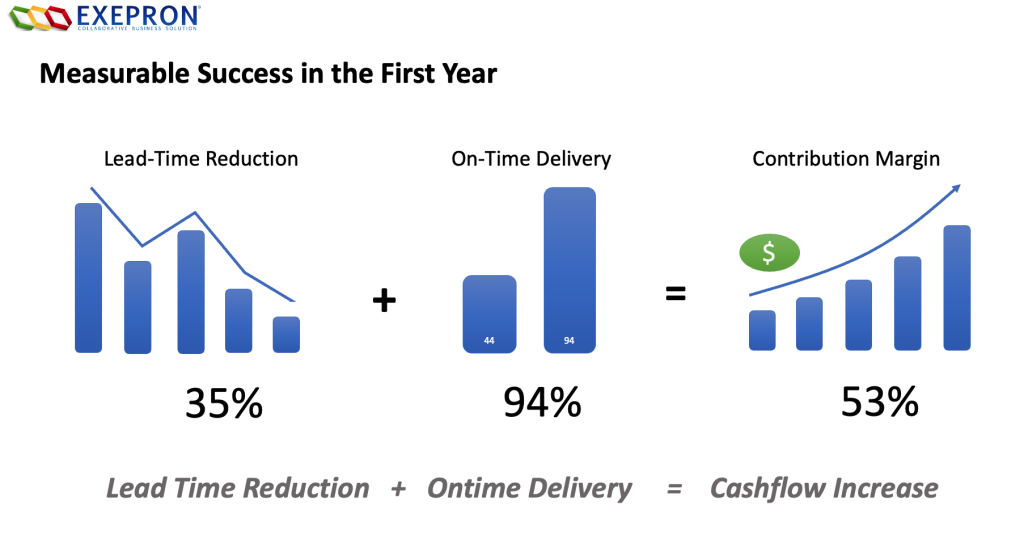

Here are real industry testimonials on lead-time reduction and on-time delivery.

Why?

Most organizations manage their operations in ways that unintentionally slow flow.

Work is released into the system too early.

Resources are scheduled for local performance rather than for system-wide performance.

Managers attempt to maximize utilization rather than protect flow.

Uncertainty is treated as something to eliminate rather than something to manage.

The result is predictable: congestion, expediting, unreliable delivery, and longer lead times.

But every operational system has something else as well:

A limitation, and more importantly, a prioritized sequence of multiple limitations. Each limitation in the system ultimately determines how much work the entire organization can complete.

When leaders identify these limitations and manage the entire system around them, something powerful happens.

Flow accelerates.

Uncertainty becomes manageable.

Work moves predictably through the system.

Lead times shrink—often far more than the 20% improvement used in the example above.

And when lead times shrink, the economic effects compound.

Inventory falls.

Asset productivity increases.

Contribution Margin or Throughput rises.

Cash flow improves.

Unit costs decline naturally.

This is the economic power of a logistics strategy.

Not cutting costs.

Not squeezing margins.

By accelerating the rate at which assets convert capital into revenue.

Organizations that understand this do not simply survive margin pressure—they outperform it.

And the starting point is simple:

Discover the system’s limitations, manage the uncertainty around them, and allow flow to accelerate.

Because when flow improves, the entire economics of the business improves.

Download an MS Excel Model Here and Test the Lead Time impact on your Organization.

Click on the Link.

LeadTime-Impact-Model-V2-Mar11-1 (11)

About the Author

John L. Thompson is COO and co-founder of Exepron and a practitioner of the Theory of Constraints with over 40 years of experience helping organizations improve flow, reduce lead times, and increase Asset Productivity.

email: JohnT@Exepron.com

Exepron: for Logistic-Driven Organizations.

Find out how to significantly reduce lead time and provide reliable delivery at exepron.com

Let’s explore if there’s a fit for your organization.

We invite you to test the Exepron. We’ll bring the method, platform, and support. You bring the willingness to differentiate, retool operations, and lead cohesively.